Why India’s oldest private telco may still be its most underrated compounder.

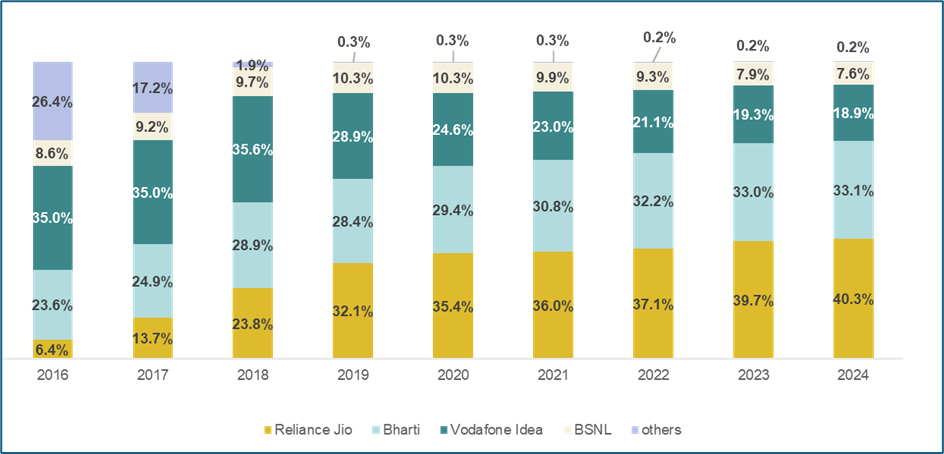

In 2016 Reliance Jio declared voice calls free and data nearly free. Industry ARPU (Average Revenue Per User) crashed from ~₹250 to under ₹100 and ten operators disappeared within three years.

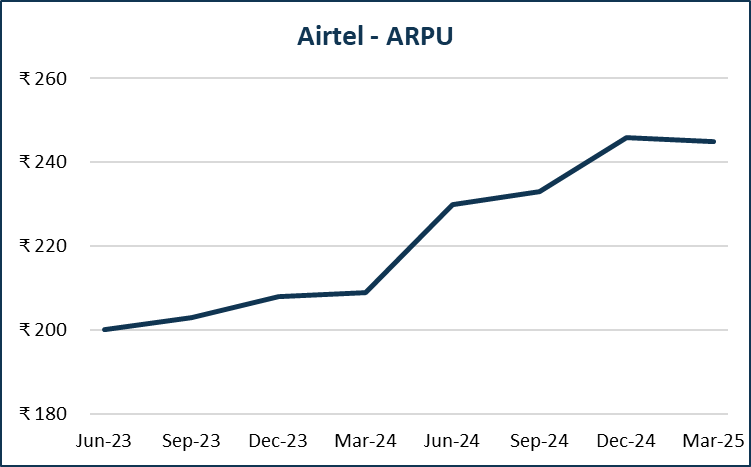

Yet in FY25 Airtel has hit an all‑time‑high 33 % wireless market‑share and a sector‑leading ARPU of ₹245.

Airtel didn’t just survive. It grew, consistently.

How did a company many wrote off become India’s most profitable telco and why could the next decade be even better? Below we retrace the bigger picture, unpack Airtel’s playbook, map the runway ahead and flag the risks investors must watch.

1. Airtel’s Playbook for the Post‑Jio Era

Premium‑First Positioning

While rivals chased low‑value subscribers, Airtel pruned its base and doubled down on higher‑income, data‑heavy users. The result is the highest ARPU in India (₹245 in Q4 FY25), now almost 35 % above Jio.

Network & Experience Edge

- Rapid 5G rollout across 5000+ cities

- 489,000 rkms fibre, delivering best latency

- AI‑led service stack converts prepaid to sticky post‑paid

Diversifying Cash Engines

- Enterprise & IoT: Over 54 % share of India’s M2M SIMs gives Airtel a toll‑road on connected‑device growth.

- Nxtra Data Centres: Airtel’s subsidiary Nxtra has 12 % market‑share of data centres in India today. Another 400 MW fresh capacity under build will likely double revenue within 24 months.

- Africa: Airtel’s Africa business is now 25 % of its topline and growing twice as fast as India, de‑risking currency and regulation.

- Digital Adjacencies: Cloud, CPaaS, cybersecurity and Airtel Payments Bank are tracking 25‑30 % CAGR as per management guidance.

Capital Discipline

- FY25 operating cash flow reached ~₹1 lakh crore

- Net‑debt/EBITDA has fallen below 2× after aggressive spectrum pre‑payments

- Expected reduction in 5G capex means each rupee of incremental EBITDA can increasingly drop to free cash flow

2. Why the Runway Is Longer Than It Looks

- Tariff Headroom

Even after recent hikes, India’s mobile ARPU is just US $1.8 vs US$30‑40 in developed markets. Pricing power of a comfortable duopoly is only beginning to show. - Data‑Centre Super‑Cycle

AI workloads, cloud migration and stringent data‑localisation rules put Airtel’s Nxtra in the slipstream of a $4 billion domestic Data Centre market growing >20 % CAGR. - Rural Upside

Two‑thirds of future subscriber growth is expected to come from rural India. Airtel already has one million retail outlets and has launched budget fixed‑wireless AirFiber for hinterland homes. - Optional IPOs

Nxtra and Airtel Africa’s mobile‐money arm could unlock significant value, recycle capital into core networks, and further deleverage the balance sheet.

3. How It Scores on Fynvestor’s CRAFT Lens (Quick‑Fire)

C – Competitive Advantage

Spectrum depth, regulatory licenses, nationwide fibre network, integrated digital suite and a sticky enterprise stack create entry barriers that are very hard and expensive to replicate.

R – Right Promoters

The promoter group continues to hold a commanding 52% stake, ensuring strong skin in the game. Public shareholding remains minimal at ~2.75% (as of Mar’25), underscoring long-term institutional confidence.

At the helm is Gopal Vittal, a visionary leader with a stellar track record. Under his stewardship, Airtel navigated the brutal telecom price war, expanded into high-growth digital services, and delivered consistent operational turnarounds. His focus on cost efficiency, premiumization, and technology-led transformation has cemented Airtel’s position as the most resilient telecom operator in India.

A – Accounting & Financial Strength

- Robust Cash Flow Generation

Airtel’s CFO/EBITDA consistently exceeds 1, supported by steadily rising free cash flows—even during the intense telecom price war. Today, it stands as a cash-generating powerhouse. - Capex Moderation & De-leveraging

With capital expenditure on a downward trajectory post-5G rollout, the company is well-positioned to accelerate debt reduction, further reinforcing its already improving balance sheet. - Enhanced Capital Efficiency

Return ratios continue to improve, with ROCE at 15.4% and ROE at an impressive 28.3%, reflecting strong operational performance and prudent capital allocation.

F – Fair Valuation

Trading at ~14.6 × FY-25 EV/EBITDA and ~40 × trailing P/E, a modest premium that’s supported by double-digit free-cash-flow growth, rapid deleveraging, and hidden optionality from potential Nxtra DC and Airtel Africa spin-offs.

T – Track Record of Leadership

Added 8 percentage points of wireless market share (from ~24 % in FY-17 to ~32 % in FY-25) while a dozen rivals vanished and industry tariffs fell to zero, underscoring Airtel’s execution edge in the toughest competitive cycle Indian telecom has ever faced.

4. Key Investment Takeaways

- Pricing is destiny in telecom. With only two serious private players left, disciplined tariff hikes can translate into exponential cash generation.

- Digital adjacencies convert a utility into a tech platform with higher multiples.

- Strengthening balance sheet provides fire‑power for strategic bets (satcom via OneWeb, enterprise cloud buys, etc.).

5. Key Risks & Watch‑outs

| Risk | Why It Matters |

|---|---|

| Regulatory overhang | AGR dues, spectrum fees, price controls or forced tariff caps could compress margins |

| Competitive retaliation | A fresh price war (e.g., Jio satcom bundling or a Vodafone‑Idea bailout) could stall ARPU growth |

| Macro / Consumption Slowdown | Any dip in discretionary spend hits prepaid recharges and data upsell |

| Tech disruption | Rapid transition to 6 G / Open-RAN might require new cap-ex cycle earlier than planned |

| Leverage & Currency | High Debt/Equity; Africa earnings sensitive to local FX devaluation |

| Cyber‑security & data privacy | Breaches could lead to fines, churn and reputational hit, especially as Nxtra scales. |

6. Fynvestor Summary

Bharti Airtel is the classic “pipes + platform” enabler: a capital-hungry network that, once built, spews operating leverage. Regulatory licences and spectrum walls forge a strong moat, while the Africa fintech arm and enterprise cloud services add multi-engine growth. With 5G roll-out nearly done, free cash generation should rise just as tariff hikes flow through. Watch the AGR overhang and debt, but the underlying engine looks primed to compound for years.

“Lay miles of fibre, plant thousands of towers, and patience turns sunk capital into a perpetual toll-booth for every byte that travels.”

Disclaimer: This article is for educational purposes and does not constitute investment advice. Please consult your investment advisor before acting on any information here.

Ready to Put Insight into Action?

Fynvestor turns deep‑dive research like this into tailored, conviction‑driven portfolios for serious wealth builders.