Rarely do tax, monetary, and fiscal reforms align in one moment. With GST 2.0, lower income tax, and sliding interest rates, India may have just lit the fuse for its next consumption supercycle.

When India first rolled out the Goods and Services Tax (GST) in 2017, it was called a “Good and Simple Tax.” In reality, it was a complex compromise with compliance headaches and endless disputes.

Eight years later, GST 2.0 is the true reset.

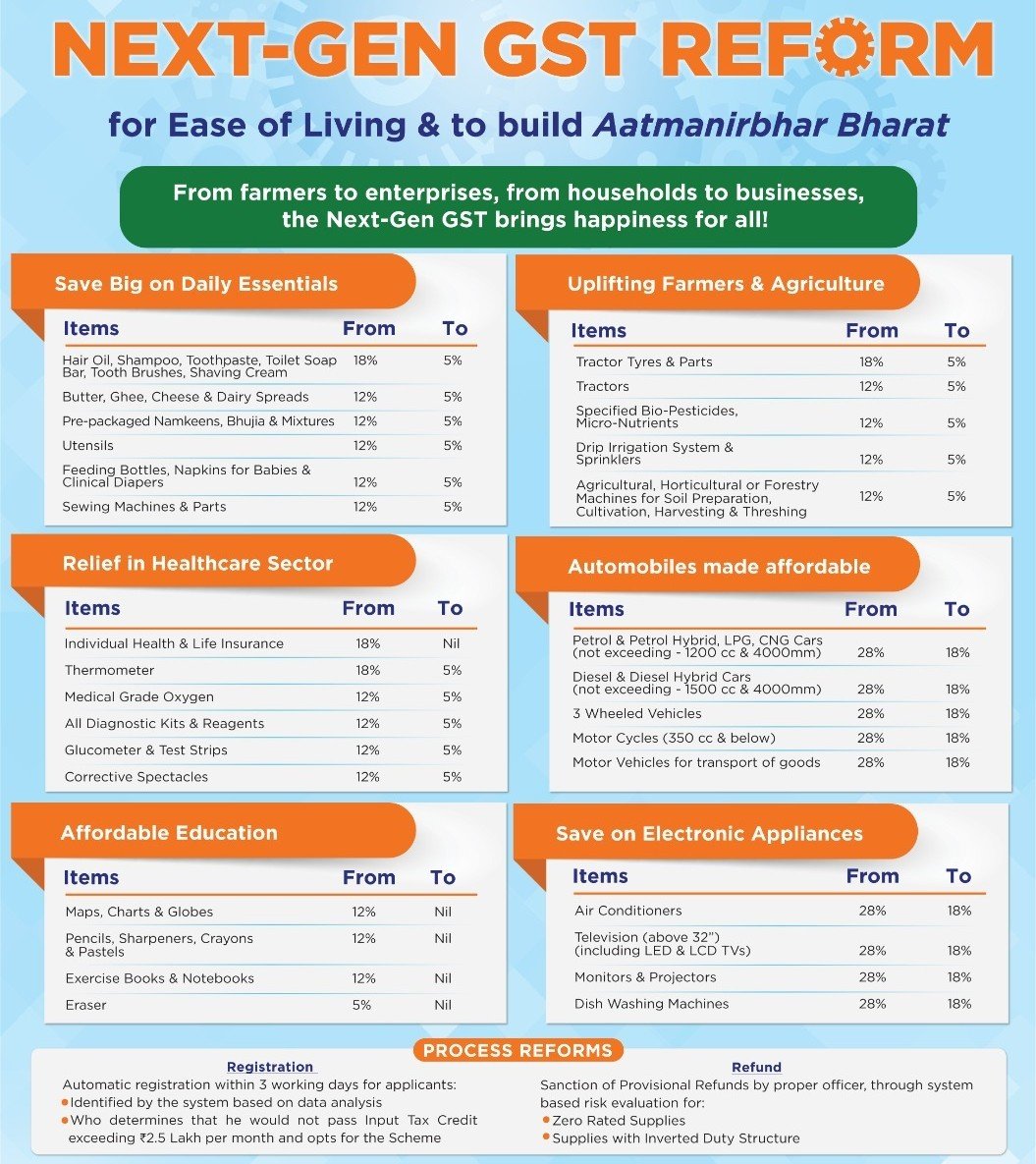

From September 22, 2025, India will collapse its four slabs into a simpler structure:

- Nil Rate for essentials (food staples, life-saving drugs, health & life insurance)

- 5% Merit Rate for mass-market goods (packaged foods, soaps, tractors, textiles)

- 18% Standard Rate for most goods & services (consumer durables, small cars, cement)

- 40% Demerit Rate for luxury and sin goods (SUVs, premium bikes, tobacco, online gaming)

1. Triple Stimulus

GST 2.0 is just one piece of the puzzle. In the same year, the government has:

- Reduced personal income tax rates for the middle class

- Cut interest rates, as lower inflation gives RBI room to ease

Put together, this is a three-pronged consumer stimulus:

- More money in hand (lower income tax).

- Cheaper access to credit (lower interest rates).

- Lower product prices (GST cuts).

Together, these reforms create a perfect storm of affordability: more money in wallets, lower financing costs, and cheaper goods on shelves. This rare alignment could unlock India’s next consumption supercycle.

2. Rural Demand: The Unsung Hero

The rural economy is the silent powerhouse that could see the biggest boost.

- Tractors & farm machinery GST cut from 12% to 5%.

- Agri inputs & irrigation equipment also moved down to 5%.

- Cheaper inputs → lower farm costs → higher disposable income.

At the same time, rural consumers will pay less for everyday essentials (soaps, packaged foods, oils, and toiletries, all down to 5%).

This double effect: lower farming costs + cheaper essentials, could trigger a revival in rural demand, which has been weak in recent years.

Investor Takeaway: Two-wheelers, tractors, FMCG, and rural lenders stand at the heart of this revival. Companies with deep rural penetration (like TVS, M&M, Dabur, HUL, Small-Finance Banks) are best positioned to benefit from the revival.

3. The Bigger Picture: Consumption → Capex

The first-order impact of GST 2.0 is obvious: cheaper products and higher consumption. But the second-order impact is far more powerful.

- Lower prices on autos, durables, and FMCG trigger volume growth

- Higher volumes lift factory utilization rates

- Higher utilization gives companies confidence to invest

- That confidence restarts the private capex cycle, dormant for more than a decade

Investor Takeaway: For years, government capex carried the burden. GST 2.0 can finally unlock private-sector animal spirits.

4. Affordable Housing: Cementing India’s Growth

A 10% GST cut on cement (28% → 18%) lowers construction costs by 3–5%. Combined with lower home loan EMIs (thanks to falling rates), the affordable housing segment could finally revive.

For developers, GST 2.0 improves project viability. For homebuyers, lower costs make ownership achievable, especially in Tier-II and Tier-III cities. The ripple effects include jobs in construction, higher demand for building materials, and consumption growth once families move into new homes.

Investor Takeaway: Cement majors, affordable housing developers, and housing finance companies can witness durable multi-year growth.

5. Credit Growth: Fuel for Banks and NBFCs

Consumption booms don’t happen without credit. With lower GST and interest rates, demand for:

- Auto loans (cars, two-wheelers, tractors)

- Consumer durables financing (appliances, electronics)

- Housing finance (especially affordable housing)

will accelerate sharply.

This could lead to a prolonged double-digit credit growth cycle.

Investor Takeaway: The winners of GST 2.0 will not just be FMCG, consumer durables or auto manufacturers, but the lenders financing this wave – top private banks, small finance banks, NBFCs

6. Formalization 2.0: The Silent Wealth Creator

Lower tax rates + simpler compliance reduce the incentive for MSMEs to stay informal.

This will structurally shift market share to organized, listed players across FMCG, durables, and retail. It’s the same playbook we saw post-GST 1.0 in paints and branded apparel, only bigger.

Investor Takeaway: Focus on companies with deep rural distribution. They are best placed to capture market share as informal players lose edge.

7. Deepening Financialisation

The complete GST exemption for life and health insurance premiums is a massive catalyst. The improved affordability will drive higher penetration of insurance products, channeling household savings away from physical assets and towards financial instruments.

This benefits not only insurance companies but also the broader financial ecosystem, including asset management companies, wealth managers, and banks that thrive on a growing pool of financial savings.

8. Risks Worth Watching

- Transmission risk: Companies in oligopolistic sectors may not pass on full benefits to consumers

- Transition hurdles: Input Tax Credit adjustments for existing inventory may disrupt supply chains

- Fiscal paradox: Tax revenue loss estimates range from ₹3,700 crore to ₹48,000 crore. If collections falter, the government may scale back public capex

Final Word: The Reset Investors Can’t Ignore

GST 2.0 is not just a “Diwali gift.” It is India’s strategic bet on domestic demand. A tax architecture designed to trigger consumption, unlock credit growth, revive affordable housing, and restart the private capex engine.

The potential impact on economic growth is significant. A consensus of economic forecasts projects a direct boost to real GDP growth, with estimates ranging from a conservative 20-30 basis points to a more sanguine 100-120 basis points over the subsequent four to six quarters. A simplified, two-rate GST system will significantly enhance the ease of doing business by reducing classification disputes, litigation, and compliance burdens.

At Fynvestor, we see GST 2.0 not as a one-time boost, but as the ignition point of a decade-long transformation.

The markets will celebrate cheaper goods and higher consumption, but real wealth will be created in the sectors that capture the second-order effects.